Interactive Brokers (IBKR) was IEX’s first listing, but not for me personally.

Before joining IEX in 2015 I was responsible for Trading Floor Operations at the NYSE where I oversaw IPOs and listing transfers. The rare opportunity to launch not just a new national securities exchange, but also a listings exchange, drew me to IEX. It was a unique honor for me to be part of a team beginning to challenge an entrenched decades-old duopoly by executing our first listing…these types of opportunities don’t come around often.

It was especially rewarding because it was a chance to see our ideas about better market structure play out in practice. It was an opportunity to design technology and functionality that aligns the interests of corporate issuers, industry participants, and investors. I’m incredibly proud of the results.

You can imagine that it took a tremendous amount of planning, collaboration and hard work to launch a new listings exchange. Beyond the IEX team, several of our Member Firms supported IEX by joining our Market Making program, dedicating testing resources for our Saturday and weekday production tests, and also provided valuable feedback during our auction design process.

Let’s be clear, it has only been a couple of weeks and we continue to analyze the stock’s trading performance, but so far we are very excited and optimistic about what we’ve observed in IBKR:

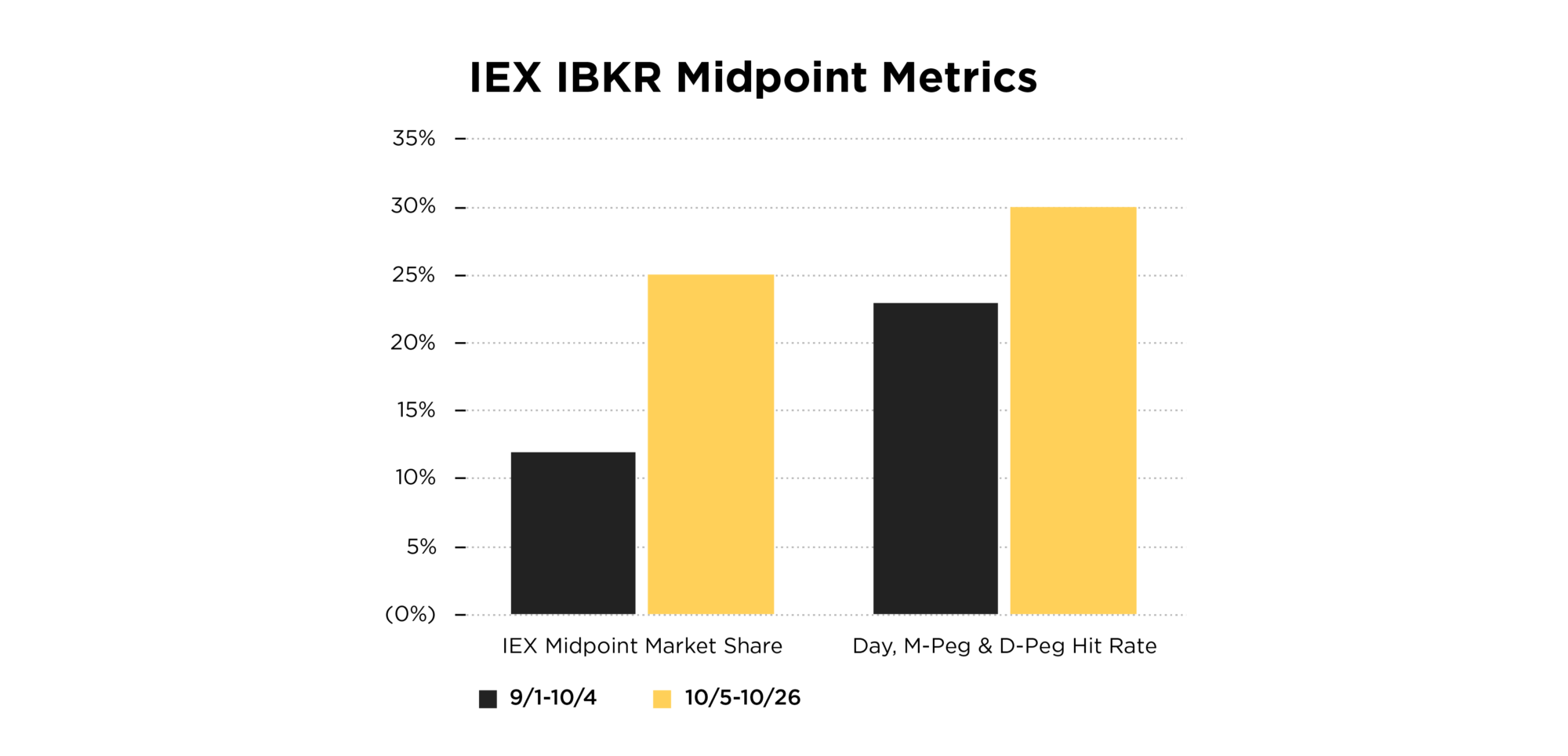

- Healthy balance between long-term and short-term participants as IEX’s market share in IBKR has grown to 30%

- Larger, more stable quotes, the opposite of what you typically see during volatile markets

- Better execution quality for IBKR shareholders trading on IEX, because more midpoint trading is protected by IEX technology

A Market for All

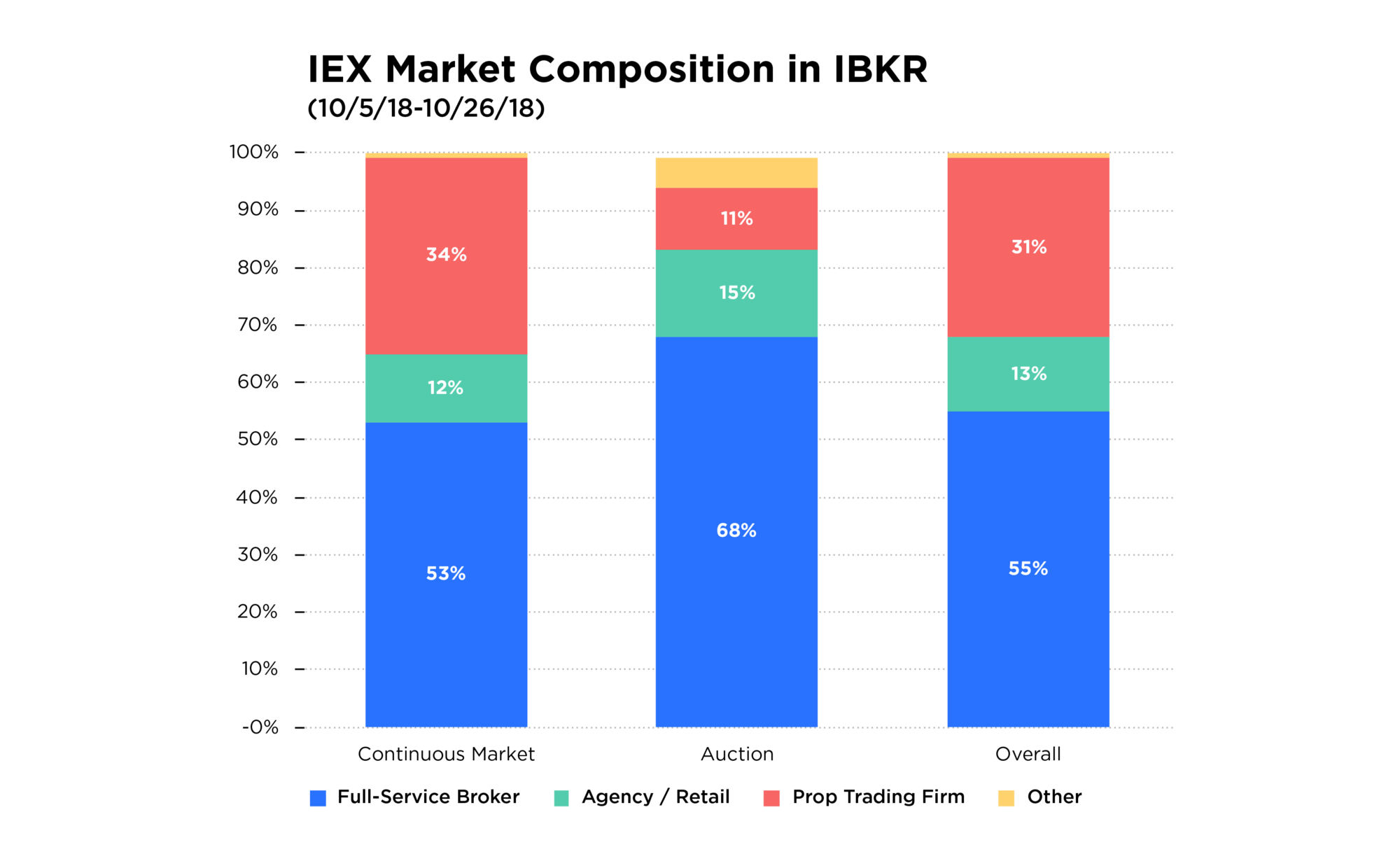

IEX’s balance of industry participants has always differentiated us from other exchanges: long-term investors trust us because of our technology, but we also attract the right type of short-term trading. As IEX’s market share in IBKR has grown, we were pleased to see that the diverse mix of participants in IBKR held firm: more than two-thirds of our volume has come from full-service, agency-only and retail brokers representing natural investors while one-third is proprietary trading firms. This is nearly the inverse of what happens on other markets — so we believe that it’s a better and more stable mix of participants trading on different time scales.[1]

Specifically, we see nearly 90% of participation in opening and closing auctions is from agency and full-service broker dealers, with the balance coming from proprietary trading firms who are helping to offset auction imbalances and discover the most efficient clearing price — which is reflective of a healthy ecosystem.

More Size and Stability in IBKR’s Quote

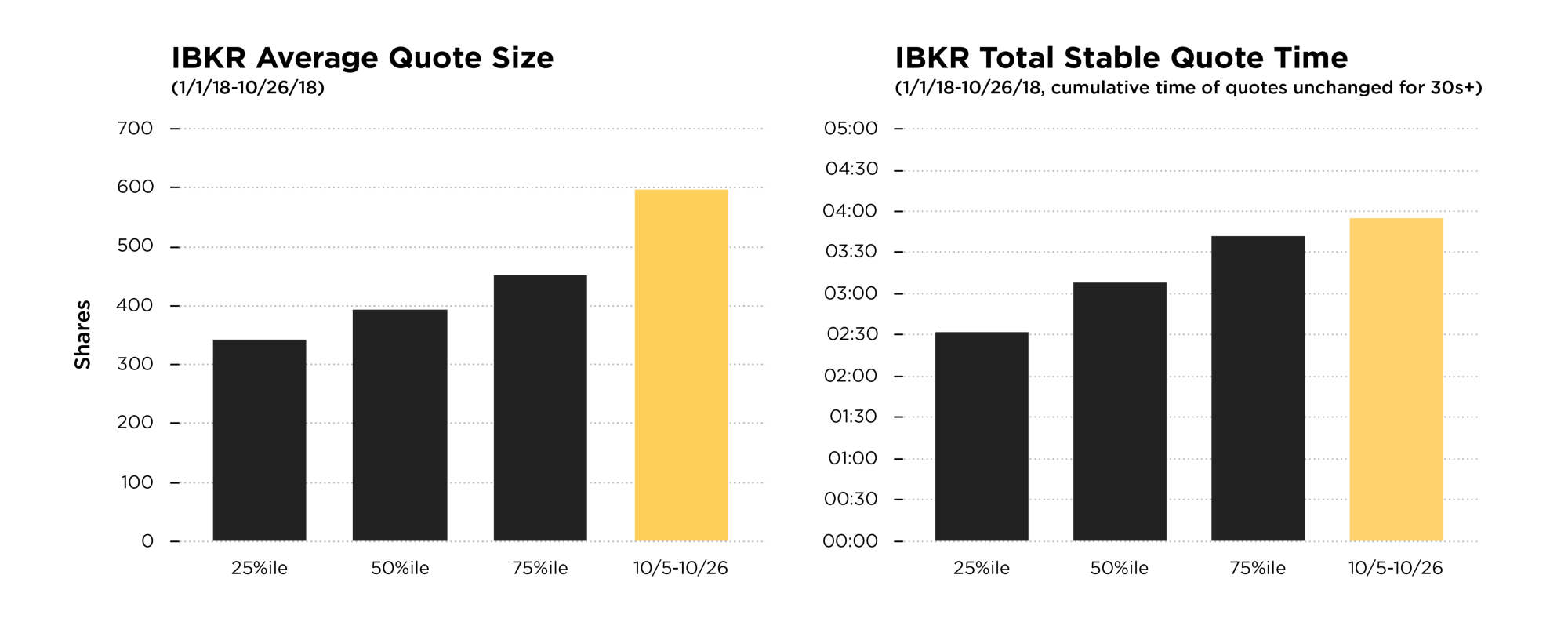

Since IBKR transferred to IEX, the stock’s quote has grown larger and more stable. In fact, the quoted size has grown by nearly 50% when comparing IBKR’s quote size since switching to IEX, versus the rest of 2018. Keep in mind, that in volatile markets, displayed quote size tends to decrease — so we are encouraged by this early result.

This increase in IBKR’s quote size also comes with (and is likely related to) more stable and durable quotes, defined as periods where the National Best Bid and Offer (NBBO) doesn’t change for at least 30 seconds. We imagine this is a welcome sign to most corporate issuers, especially when markets are as volatile as they’ve been in recent weeks! While it’s still early days, it’s affirmation that IEX’s unique design can improve the liquidity dynamics of IEX-listed securities

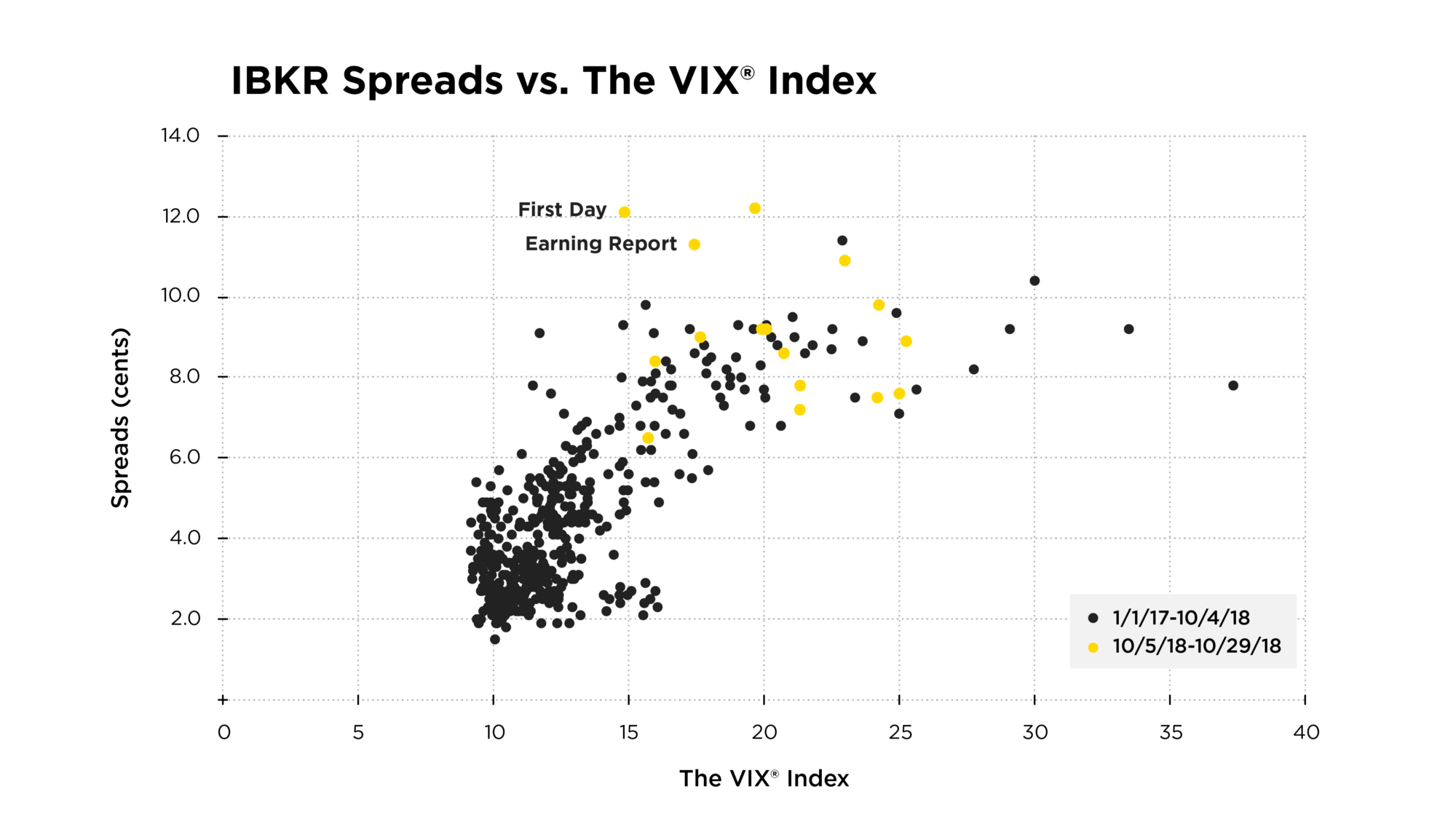

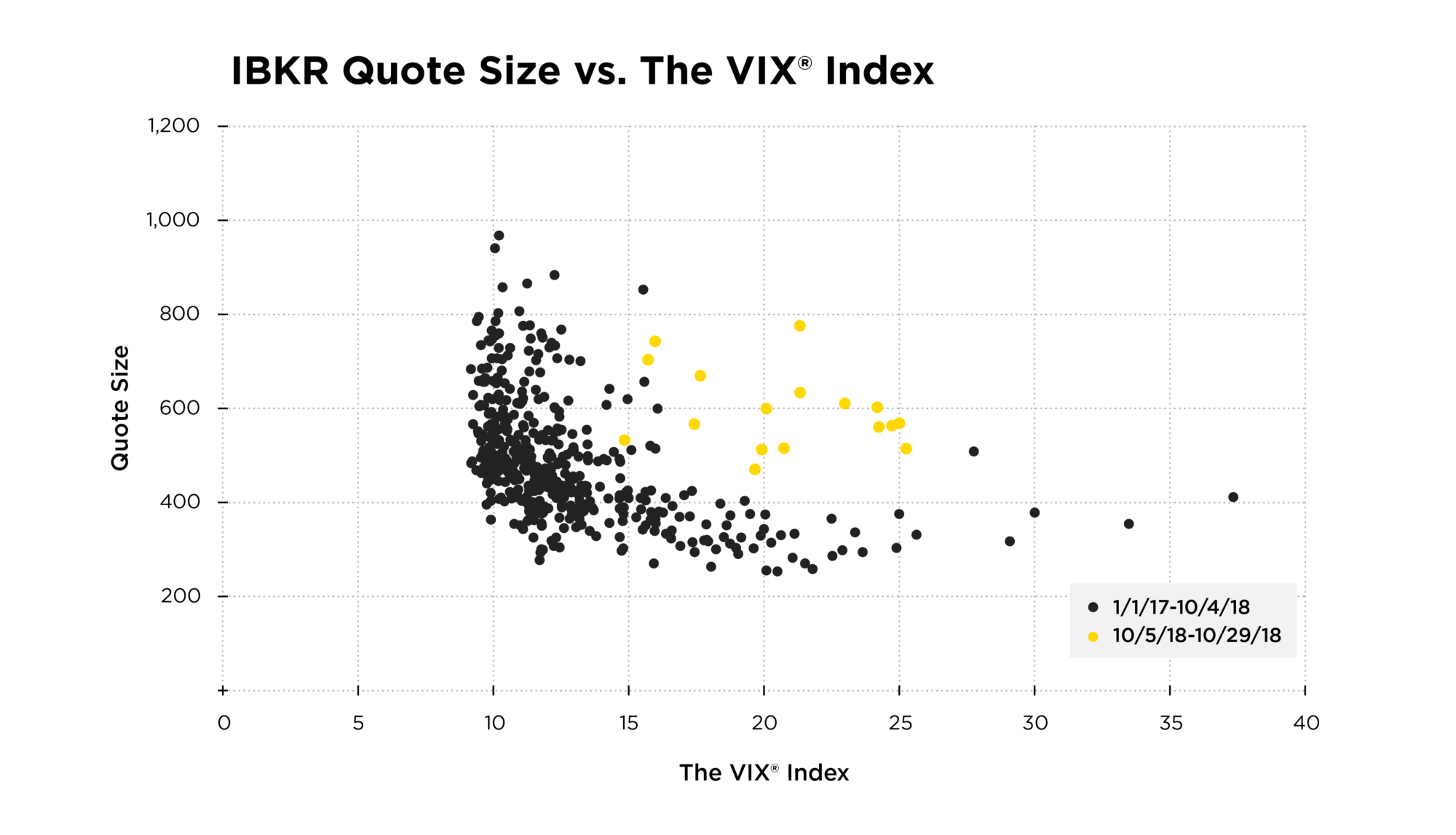

Any trading practitioner will tell you that the recent stretch of volatility will have an impact on statistics — and it has been a primary factor in driving an increase in spreads for many stocks, including but not limited to IBKR. This relationship becomes apparent when you plot The VIX® Index (a popular measure of volatility) against IBKR’s spreads. As you can see from the chart below, the wider spreads in IBKR since the switch to IEX historically correlate to The VIX® Index. It’s also important to remember that a tighter spread, of smaller size, isn’t necessarily helpful to large investors who have more than a few hundred shares to buy or sell!

So what’s truly striking is to see that IBKR’s quote since switching to IEX has increased in size during volatile markets, bucking its historical trend.

Better Execution for IBKR Shareholders

Sometimes it’s the things that stay the same that are just as impressive. IEX specializes in fair midpoint trading, which offers investors both buying and selling IBKR price improvement compared to the NBB/NBO.

IEX’s market share of midpoint trading in IBKR doubled to 25% as our overall market share in IBKR grew to nearly 30%. This means that core behavior on IEX — long-term investors willing to trade, in large size, at the midpoint — continues.

More midpoint trades occurring on IEX means more opportunities for IBKR shareholders to buy lower and sell higher on an exchange with technology specifically designed to improve execution quality, such as reducing the market impact of their trades.

Better is Possible

IEX is already thinking of ways to improve our performance as a listings exchange. One way we can improve is by encouraging increased participation in our open and closing auction by broadening access to data. Currently auction information messages are not available on the cheaper, public data feed. IEX actually proposed augmenting the CTA SIP to carry this information but unfortunately there are exchanges who do not want this information available to the public as it decreases the value of their own proprietary data feed. (For more information read Nasdaq’s letter to the SEC opposing our use of the CTA SIP to disseminate auction information over the public feeds into the hands of more investors — anyone who heard their comments during last week’s SEC Market Data Roundtables heard this live and in real time!). But hopefully, with current scrutiny on SIP governance, this can one day be a reality.

I’m excited by the possibilities that lie ahead for our listings business and for other IEX-listed companies. While it’s still early days for IBKR listed on IEX, we see the potential for a more representative blend of participation, better quote stability for the issuer, and better effective spreads for investors and traders. Better markets aren’t just theoretical…we, along with visionary leaders like IBKR, and with the help and support of industry participants and our Members, believe it’s something we can all experience soon.

[1] References to participant-types and categorizations are based on broker MPID self-classifications.